We’ve received a lot of questions and concerns from our individual and small group clients about the big jump in rates for their 2018 renewals. While there are several contributing factors (insurance trend/inflation, everyone’s a year older than they were last year, etc.), the number one reason for the premium spike is the new rating methodology for children under the age of 21.

New Rating Factors

The Affordable Care Act called for 3 to 1 age rating in the individual and small group markets. Basically, the rate for a 21-year-old is set at a factor of 1.0 and everyone else’s premiums are a factor of those rates. The factor for someone age 40, for instance, is 1.278, meaning that his or her rates will be 27.8% higher than the 21-year-old’s rates. The factor for a 46-year-old is 1.5; it’s 2.04 for a 53-year-old; and it maxes out at 3.0 for a 64-year-old.

Until now, the rating factor for anyone under age 21 was .635, meaning that children were charged just under two-thirds the amount that a 21-year-old was charged. Not anymore.

New regulations issued by the Department of Health and Human Services at the end of 2016 changed the way children are rated on both individual and small group plans, increasing the rating factor from .635 to .765 for children age 14 and under and then applying one-year age bands with higher rating factors each year after that. The effect has been huge and very negative for families with children and small employers with a lot of children on their health plan.

Example

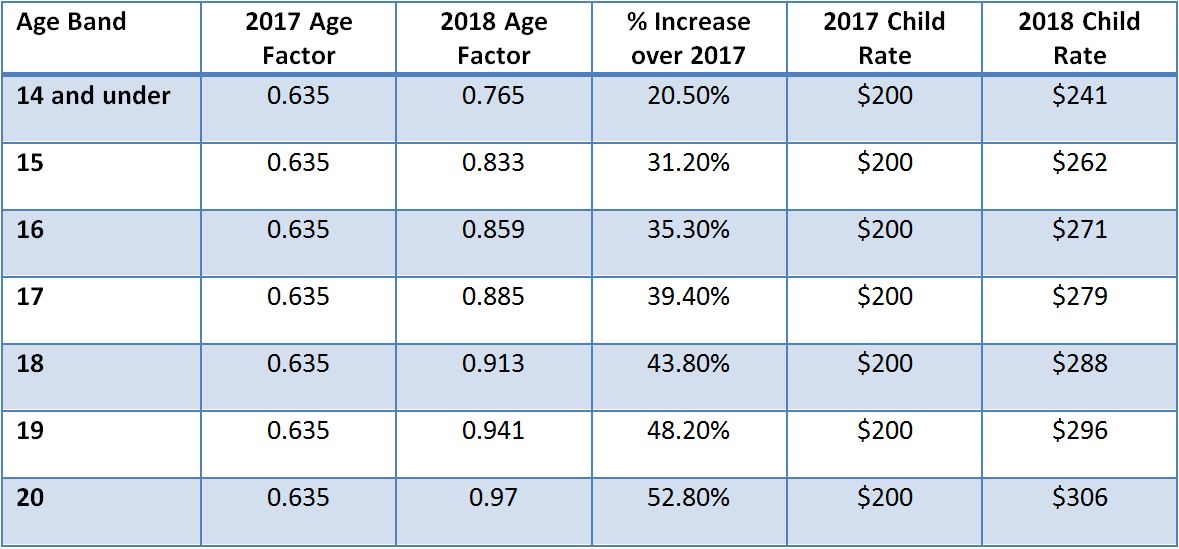

As an example, if the rate for a 21-year-old was $315 in 2017, the rate for children and young adults under age 21 was $200. Here’s the math: $315 x .635 = $200.

In 2018, that same $315 rate for a 21-year-old would lead to premiums ranging from $241 for children 14 and under up to $306 for a 20-year-old. In other words, child rates based on age alone have increased by 20% to 52%, and even more when we apply the normal annual trend increase.

This table shows the new age rating factors and illustrates the jump in premiums from 2017 to 2018.

Why did HHS change the rating factors?

The short answer is that we don’t know. In the final regulations, the Department of Health and Human Services says that the adjustment is necessary to better reflect the actuarial risk of children and to provide a more gradual transition from child to adult age rating. In other words, kids cost more than the government originally thought they did. It’s possible that free up-front preventive care and lots of immunizations, ADHD diagnoses and medication, and the opioid epidemic and substance abuse treatment are all contributing to the higher claims cost for children.

Families

For families with children, especially families with multiple teenage children, the new rating factors have caused premiums to skyrocket. Unfortunately, there aren’t a lot of solutions, but there are a couple options:

- One, of course, is to buy a plan with less benefits. Usually this means a plan with a higher deductible, higher out-of-pocket limit, and no up-front copayments for doctors and prescriptions.

- A second option, if the family owns a small business, is to purchase a small group policy instead. This can be done at any time of the year; it’s not restricted to the annual open enrollment period.

Small Employers

For small employers, offering plans with more cost-sharing is also an option. It might also be worth considering a move to age rating rather than composite rating at renewal time. When a plan is composite rated, the group is charged an average premium for employees and dependents:

- the employee + child(ren) rate is two times the employee rate,

- the employee + spouse premium is two times the employee rate, and

- the family premium is three times the employee rate.

With age rating, each employee is charged the appropriate premium based on his or her age and number of family members covered. This will cost employees with large families more, but it will save money for those without children on their health plan. Because employers normally base their monthly contributions on the employee only premium, it could also save the company some money.

One-Time Adjustment

According to the Department of Health and Human Services, this change to the child rating factors is a one-time event. We do not expect a similar change for 2019. Thank goodness!